The Government of India introduced a brand new Employees’ Provident Fund (EPF) Scheme in 2026. This new framework comes under the Code on Social Security, 2020. It replaces the old, decade-old regulations with a highly modernized structure. The fresh rules streamline how millions of salaried employees contribute to and withdraw from their provident fund accounts.

The main aim of this overhaul is twofold. First, it makes the advance withdrawal process extremely smooth. Second, it protects your long-term retirement corpus from draining quickly. If you are an EPFO subscriber, you must understand these changes immediately. These updates alter your access to your own hard-earned money during job changes and emergencies.

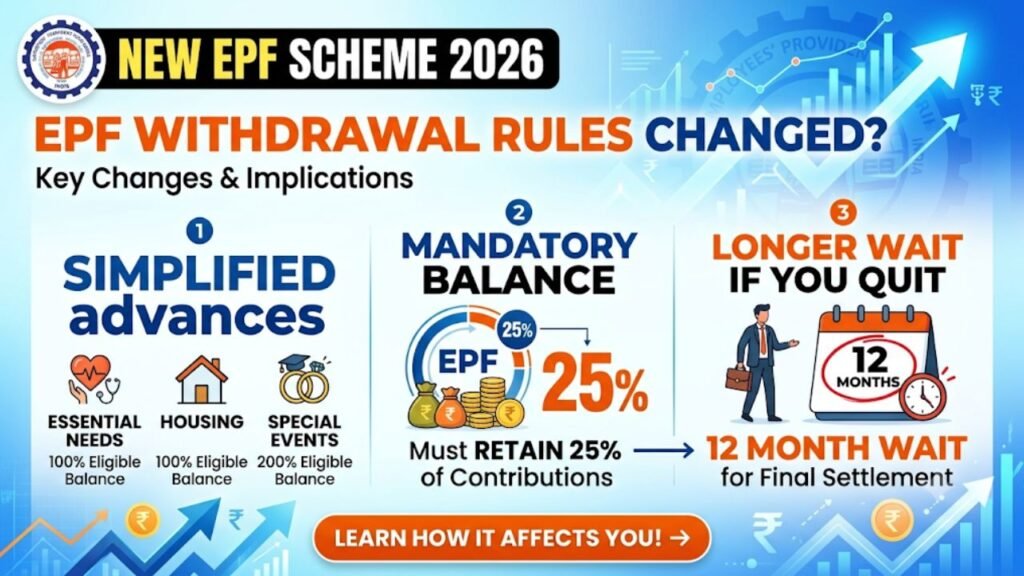

Here are the 3 major updates to your provident fund withdrawals that you must know today.

1. Multiple Advance Reasons Merge into 3 Broad Categories

Earlier, the EPFO portal displayed a long list of specific reasons for advance withdrawals. You had to select a precise clause for medical issues, marriage, home construction, or education. This complex structure caused confusion and led to frequent form rejections.

The New EPF Scheme 2026 completely removes this complicated structure. The government reduces all partial withdrawal reasons into three simple, broad categories.

- Essential Needs: This bucket covers your sudden medical emergencies, hospital bills, specialized treatments, higher education expenses for your children, and marriage costs for yourself or your dependent family members.

- Housing Needs: This category combines all real estate-related claims. It includes purchasing a new residential plot, constructing a house, buying a flat, paying off an active home loan, or renovating your existing property.

- Special Circumstances: This group handles unique emergencies. The Central Board of Trustees (CBT) updates and notifies these circumstances from time to time. It acts as a safety valve for unforeseen national or personal crises.

This categorization simplifies the online application layout on the Unified Member Portal. It reduces paperwork and guarantees faster claim settlements.

2. Mandatory 25% Balance Retention Rule

The new rules offer great flexibility for partial advances, but they come with a strict safety check. You cannot withdraw your entire EPF balance whenever you like before retirement.

Under the 2026 guidelines, subscribers must maintain a minimum balance in their EPF account during advance claims. You must retain at least 25% of your total employee contributions inside the account. This rule ensures that your core retirement fund stays intact.

For example, if your total eligible contribution stands at ₹4,00,000, you can only withdraw a maximum of ₹3,00,000 for permitted advances. The remaining ₹1,00,000 must stay inside the fund to accumulate compound interest. This rule shields your future financial security from aggressive early spending.

3. Waiting Period for Final Settlement Extends to 12 Months

This is the biggest change for employees who leave their jobs or face unemployment before retirement age.

Under the old rules, if you resigned or lost your job, you could apply for a complete final settlement of your EPF account after remaining unemployed for just 2 consecutive months (60 days).

The New EPF Scheme 2026 extends this waiting period significantly. You must now remain continuously unemployed for 12 months before you can apply for a premature final settlement.

The government wants to discourage citizens from closing their retirement accounts during short career breaks or mid-career transitions. The EPFO wants you to transfer your old account to your new employer using your Universal Account Number (UAN) instead of draining the balance completely.

Note: This 12-month restriction only applies to final full settlements. It does not block you from taking partial advances for urgent medical care or education if you meet the specific eligibility conditions.

| Feature / Rule Area | Old EPF Scheme (1952) | New EPF Scheme (2026) |

| Statutory Alignment | Run under old standalone acts. | Officially aligned with the Code on Social Security, 2020. |

| Withdrawal Categories | Dozens of complex, fragmented reasons with separate paperwork. | Simplified into 3 broad heads: Essential Needs, Housing Needs, and Special Circumstances. |

| Final Settlement Wait Time | Allowed after 2 months of continuous unemployment. | Extended to 12 months of continuous unemployment before full premature final withdrawal. |

| Minimum Balance Rule | No uniform cap; subject to individual advance rules. | Mandatory 25% balance retention must stay in the account for standard advances. |

| Auto-Settlement Limit | ₹1 Lakh limit for auto-claims processing. | Increased to ₹5 Lakh under the digital-first structure. |

| Contribution Rates | Standard 12% (Employee) / 12% (Employer). | Unchanged (12%). However, emergency provisions now exist to defer during exceptional crises. |

| Statutory Wage Ceiling | Base limit set at ₹15,000 per month. | Unchanged (₹15,000); higher basic wage contributions remain voluntary. |

| Digital Verification | Heavy dependency on OTPs and physical/employer verification. | Introduces Aadhaar-based face authentication and direct instant processing links. |

Interest Rate

| Scheme Name | Interest Rate (p.a.) |

| Employees’ Provident Fund (EPF) | 8.25% (Credits hit by July 15, 2026) |

| Public Provident Fund (PPF) | 7.10% |

| Senior Citizen Savings Scheme (SCSS) | 8.20% |

| Sukanya Samriddhi Yojana (SSY) | 8.20% |

Important Dates for the New EPF Scheme 2026

The implementation follows a strict government timeline. Keep these crucial dates in mind to manage your funds smoothly.

| Event Details | Applicable Date |

| Official Ministry Notification Date | July 9, 2026 |

| Enforcement of New Withdrawal Rules | Immediate Effect |

| Mandatory UAN-Aadhaar Linking Deadline | Active Check during Entry |

Key Highlights of New EPF Rules 2026

This table summarizes the core operational transformations that impact your monthly savings and final payouts.

| Feature Type | Old Regulation System | New 2026 Rule System |

| Advance Selection Heads | Dozens of complex, specific sub-clauses | 3 clean categories (Essential, Housing, Special) |

| Minimum Account Retention | Nil for specific full advance clauses | Mandatory 25% of total member contributions |

| Unemployment Waiting Period | 2 Months (60 Days) | 12 Months (1 Year) |

| Application Process Type | Manual or multi-document verification | Digital Self-Certification via online UAN Portal |

| Withdrawal Frequency | Fixed lifetime limits per reason | Multiple annual claims based on category limits |

How to Apply for Online Advance Under the New Rules

The online application mechanism is fast. Follow these simple instructions to file your claim on the portal.

- Go to the official EPFO Unified Member Portal.

- Enter your unique 12-digit Universal Account Number (UAN) and password.

- Complete the Captcha security check and click login.

- Navigate to the ‘Online Services’ section on the top menu bar.

- Select the ‘Claim Form (Form-31, 19, 10C & 10D)’ option.

- Verify your linked bank account number by entering the last 4 digits.

- Choose the specific advance category from the new three-option list.

- Enter the required amount and upload a scanned copy of your cancelled cheque.

- Verify your identity using the Aadhaar-based OTP system to complete the submission.

Ensure that your Know Your Customer (KYC) details match your official documents perfectly. Your Aadhaar card, Permanent Account Number (PAN), and active savings bank account must share identical name spellings. Any spelling mismatch triggers an instant automatic rejection by the portal software.

Official Government References

Always verify your rules through official channels. Avoid relying on unverified third-party rumors or fake social media circulars.

| Government Authority / Resource | Official Direct Web Portal Address |

| EPFO Main Website | https://www.epfindia.gov.in |

| Unified Member Portal | [suspicious link removed] |

| Ministry of Labour & Employment | https://labour.gov.in |

Official EPFO Helpline and Support Network

If you face technical errors during online form submission or money transfer, connect with the helpdesk directly.

| Support Channel Type | Official Contact Details |

| National Toll-Free Helpline | 1800-118-005 |

| Grievance Redressal Portal | EPFiGMS Portal (https://epfigms.gov.in) |

| Official Social Media Support | @EPFOIndia (Verified Twitter/X Handle) |

Final Words for Subscribers

The New EPF Rules 2026 bring much-needed clarity to personal finance management. The simplified three-bucket advance system takes away the stress of paperwork during urgent family medical emergencies. At the same time, the extended 12-month unemployment clause forces you to build discipline. It stops you from breaking your long-term retirement safety net for short-term expenses.

If you switch jobs this year, do not apply for a full withdrawal. Generate your digital transfer request using your UAN instead. This simple habit keeps your continuous service history active and protects your tax-free interest compounding benefits for the future.